Three Emerging Models for PropCo "Seed" Investments

Real estate investors are defining their own version of venture investing, making $10mm+ commitments to seed the real estate portfolios of emerging OpCo-PropCo sponsors. But strings are attached.

Today’s Thesis Driven is a guest letter from Paul Stanton & Sandor Valner, Co-Founders and Partners at Proptech Bankers, where they advise real estate clients–including OpCo-PropCos–on structuring and capitalization.

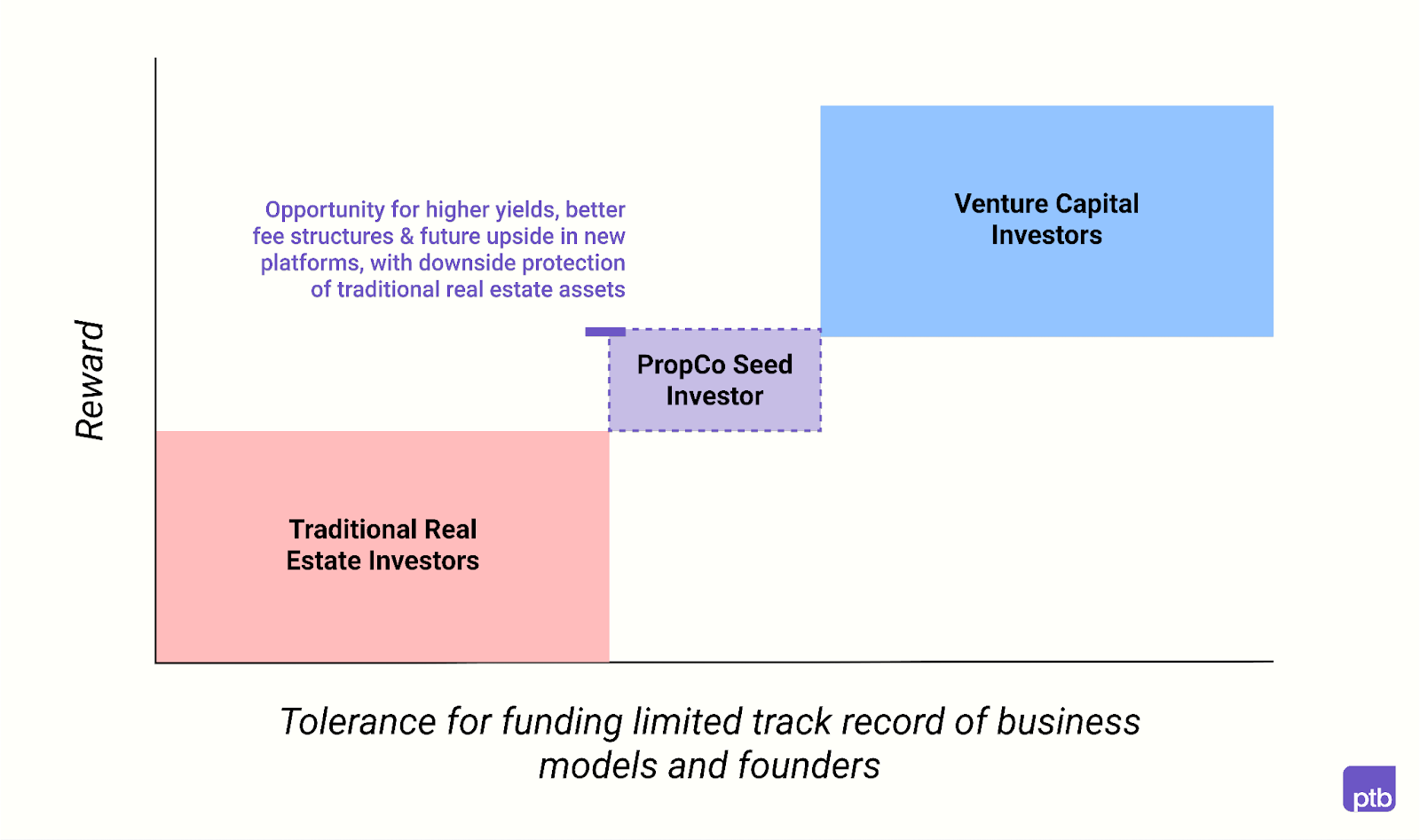

Unlike VCs, traditional real estate investors are not compensated for taking big risks on small investments. Their business models rely on consistent “singles” and “doubles” – not a few home runs. And institutional real estate investors look to deploy large checks into each thesis they embrace.

On the other hand, many tech-enabled real estate operating companies, or OpCos, cannot provide a clear path to a 5x return targeted by VCs, and their PropCos are too small and lack the track record to attract traditional real estate investors. But a handful of investors are pioneering new investment structures to capture the upside of investing early in OpCo-Propco concepts and other emerging real estate business models.

Over the past several years, some of the largest real estate investors in the world have begun allocating “small” pockets of capital for experimentation with new models. Others are vertically-integrated firms incubating new vehicles in-house. And then there are those reinventing the game, with new private equity real estate vehicles purpose-built to invest in OpCo-PropCos.

In this article we’ll explore these evolving PropCo “Seed” investment models, including:

The PropCo Seed investment, and why it’s happening

Joint venture structures with large institutional investors

In-house incubation with vertically-integrated firms

Examples of firms pursuing PropCo Seed models

Purpose-built Opco-PropCo funds

The PropCo Seed investment, and why its emerging

Macro shifts in human mobility, technology, affordability and sustainability have created an abundance of new real estate business models, e.g., coliving, short-term rentals, EV infrastructure, high density urban, rent-to-own, flex office, and many more.

But the capital markets lack a defined instrument that balances the risk and reward of funding these innovative models and the next-generation of real estate entrepreneurs behind them. Venture capital is too expensive while traditional real estate capital is too risk-averse.

So investment structures are surfacing to “seed” new models with the first $10 million to $200 million needed to to capture first-mover advantages in these emerging asset classes today without requiring real estate operators to spend 10+ years building a track record (i.e., the old-fashioned way).

In doing so, these Seed investors are capturing long-term value in the operators’ platforms while protecting against inherent near-term risks.

Model #1: Joint venture structures with institutional investors

Of the three emerging Seed models, OpCo-PropCo joint ventures with private equity real estate firms, hedge funds and family offices are the most popular today.

| A guest post by

|

| A guest post by

|